Intel reports “progress ahead of expectations” in Intel Foundry

Intel Foundry reports growing yields and strong 14A progress

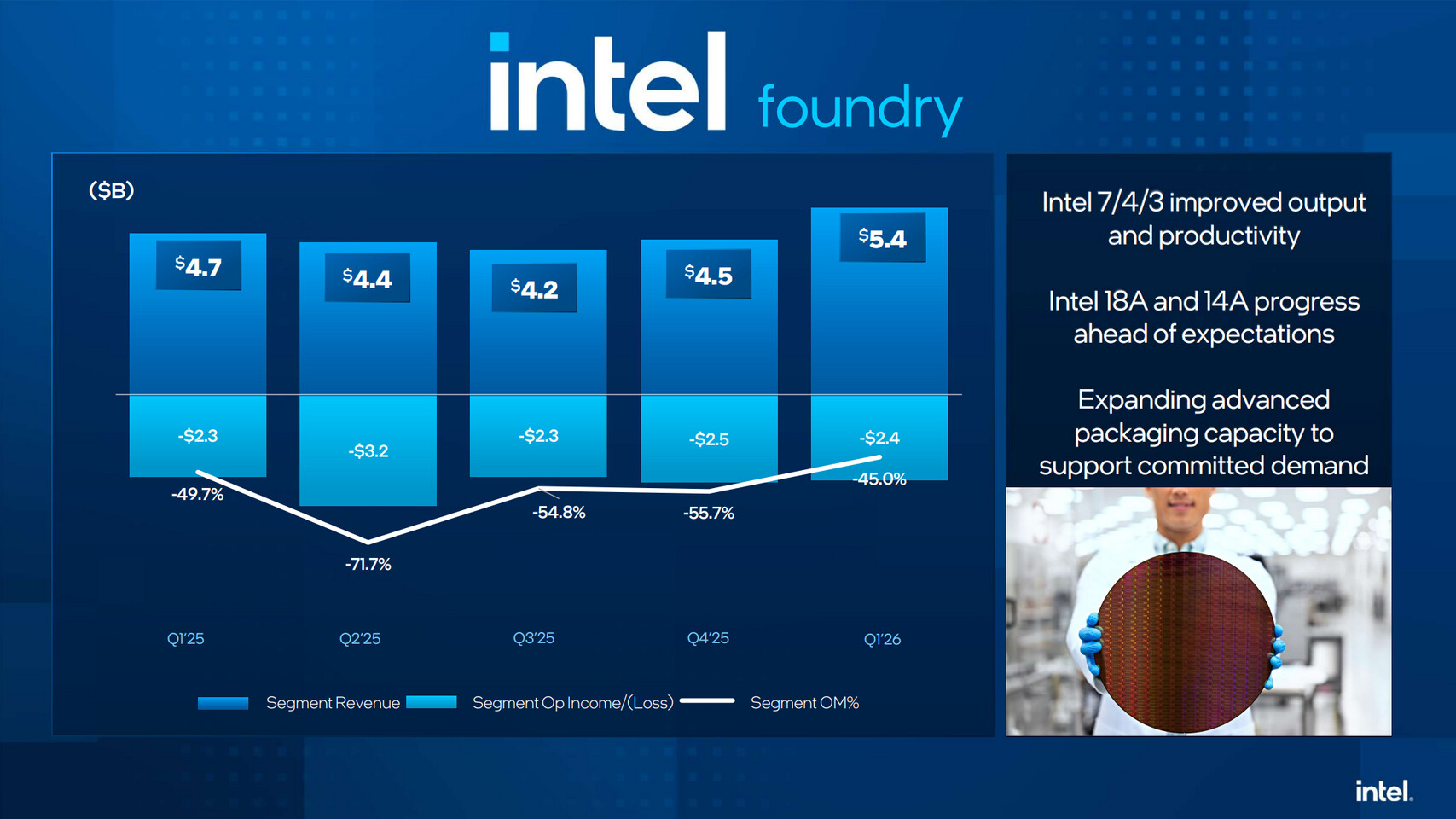

Intel has reported its Q1 2026 financials, with revenue growth, margin expansion, and higher earnings. For Intel Foundry, Intel has reported “improved output and productivity” with its Intel 7, 3, and 3 lithography nodes. Additionally, Intel has reported “progress ahead of expectations” on Intel 18A and 14A.

Intel Foundry revenue is increasing, though spending is rising as Intel invests in 14A to support “both external and internal customer evaluations”. Intel now expects Intel Foundry’s operating loss to improve this year, driven by the continued ramp of Intel 18A and further yield improvements.

Yield improvements allow Intel to produce more functional chips and to earn more per chip. This is obviously good for Intel’s financials, especially given the current CPU shortage. If Intel produces more chips, it will be able to sell them, especially if they are datacenter processors.

A year ago, the conversation about Intel Corporation was about whether we could survive. Today, it is about how quickly we can add manufacturing capacity and scale our supply to meet enormous demand for our products.

This is a fundamentally different company today, and we still have a lot of work ahead.

– Intel CEO Lip Bu-Tan

Intel’s CEO, Lip Bu-Tan has stated that Intel 14A’s node is further ahead than 18A at this part of its development cycle. He said that the “maturity, yield, and performance” are all higher. This is good news for Intel, as it wants 14A used for both Internal and external products.

Intel is currently working on Process Design Kits (PDKs) with “multiple customers” who are interested in working with Intel 14A. This includes Tesla, which plans to use Intel 14A as part of its “Terafab” project to produce AI chips. Intel’s 14A is currently at the 0.5 PDK stage. Customers will finalise volume, design, and other requirements with PDK 0.9.

Intel Foundry operating loss in Q1 was $2.4 billion, improved $72 million quarter-over-quarter as better yields across Intel 4, Intel 3, and 18A drove higher gross margins. This was mostly offset by increased operating expenses associated with an intentional step-up in Intel 14A investments to support both internal and external customer evaluations. As a reminder, Intel Foundry carries the bulk of the cost associated with the early ramp of Intel 18A, and we expect Intel Foundry’s operating loss to improve through the year as 18A continues to ramp into volume and yields improve further. Within the quarter, Intel Foundry delivered output above our expectations, drove steady improvements in yields, and met key 14A milestones.

– Intel CFO, David Zinster

Overall, things are going well for Intel Foundry. Intel is achieving higher levels of productivity with its older lithography nodes, and steady progress is being made on 18A and 14A. Intel is confident that it can get external customers with 14A. This feat would turn Intel into a true TSMC competitor and would go a long way toward pleasing investors.

You can join the discussion on Intel Foundry’s progress on the OC3D Forums.