Intel confirms Q2 losses in its latest financial reports

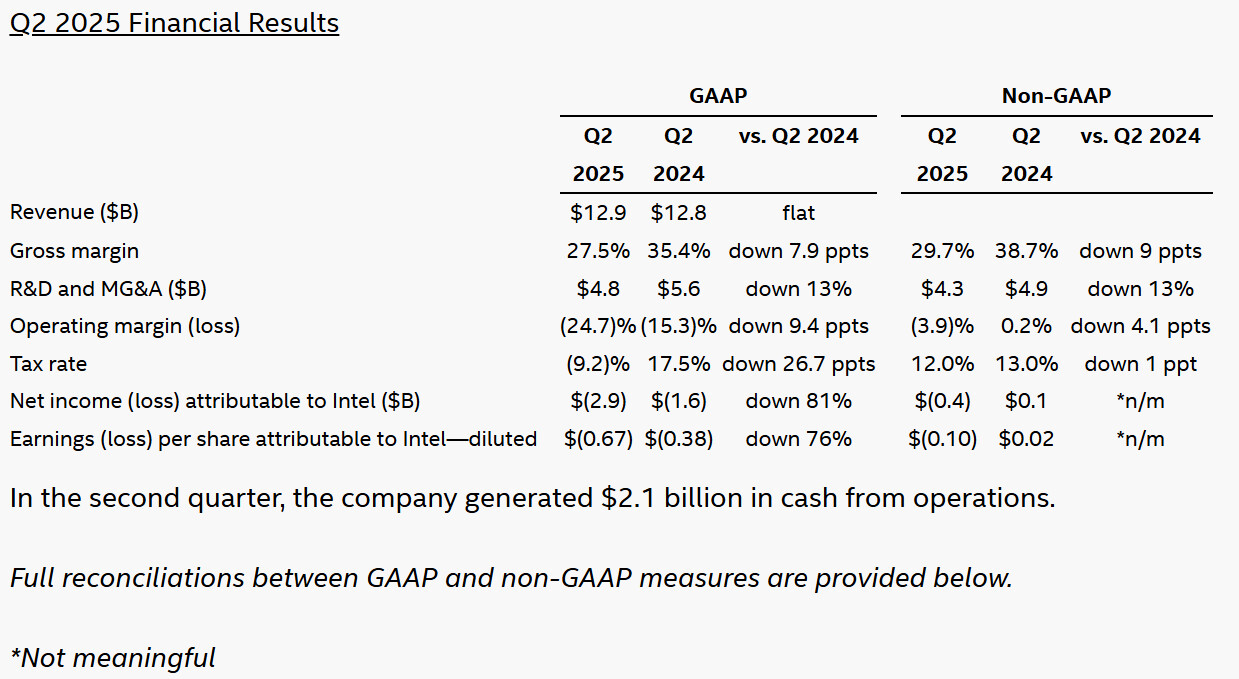

Intel confirms $2.9 billion loss in Q2 2025 as gross margins drop to 27.5%

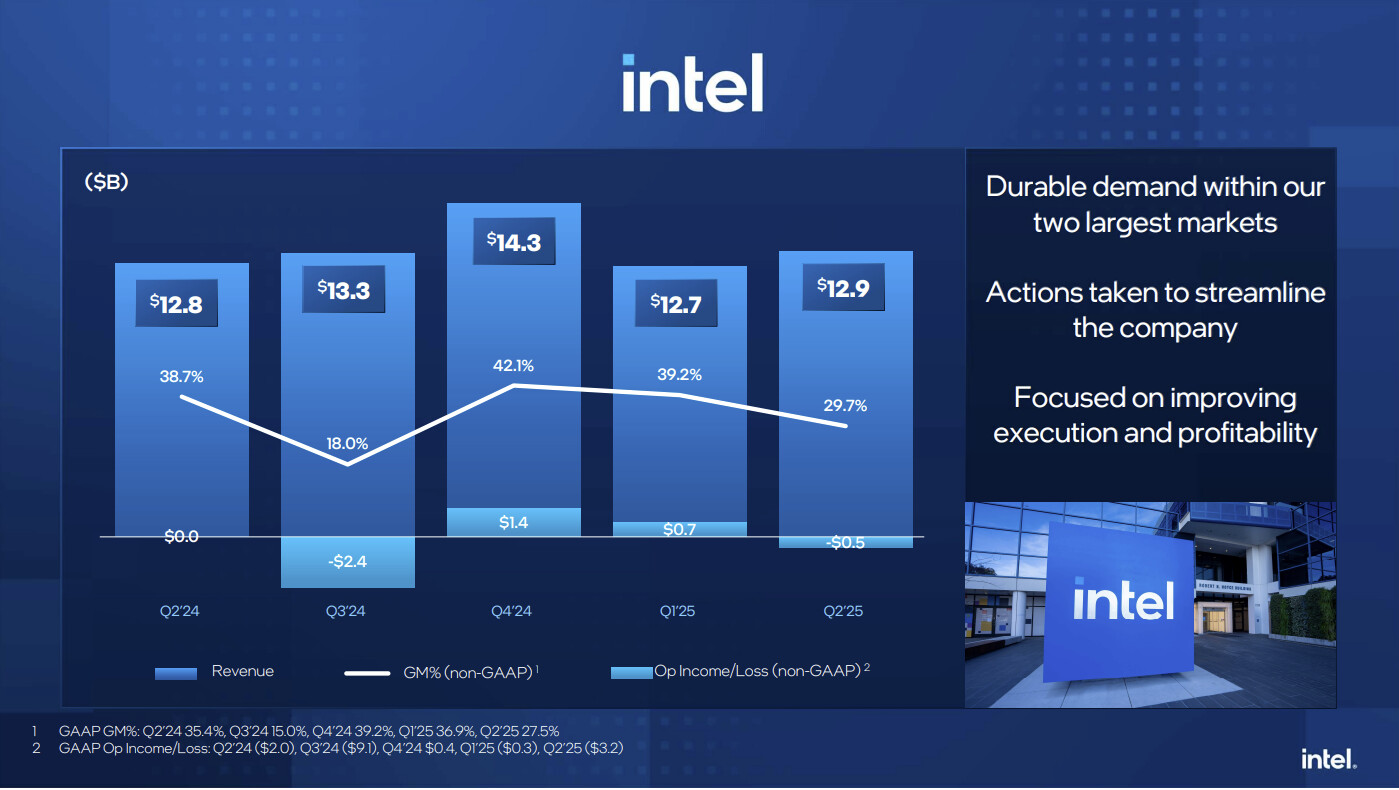

Intel has released its Q2 earnings report, and the best that can be said about it is that it could have been worse. Intel’s Q2 2025 revenue was $12.9 billion, which is slightly higher than last year’s Q2 revenue of $12.8 billion. Note that in Q2 2024, Intel’s gross margin was 35.4%. Today, Intel’s margins are 27.5%.

Intel’s CEO, Lip-Bu Tan, has confirmed that his plans to transform Intel are well underway. The company is on track to decrease its headcount to around 75,000 employees. A significant decrease from Intel’s headcount of 99,500 in late 2024. Intel has also confirmed that it has halted its plan to build fabs in Germany and Poland, lowering the company’s expenditure. Intel claims to have streamlined its management layers by 50%. This could help the company operate more smoothly in the future.

Now, Intel’s Foundry expenditure will be based on confirmed demand. Intel’s investment in its upcoming 14A node will be based on customer commitments. Intel aims to be a “financially disciplined foundry”, not a wasteful one.

Lowered margins, lowered profitability

Why has Intel made a loss in Q2 2025? The simple answer is that Intel’s margins are down. Intel’s gross margins have decreased by 9 points year over year. That’s a massive hit to profitability. For context, Nvidia’s margins are over 60%. Moving forward, Intel will need to raise its margins. This will be partially achieved by using its own 18A lithography node to produce future CPUs, reducing Intel’s reliance on TSMC. Instead of paying TSMC, Intel can use its own foundries.

Moving forward, Intel’s focus is on profitability. That means that Intel doesn’t plan to spend money on unnecessary projects. We have already seen the results of these efforts, with Intel shutting down its high-performance “Clear Linux” distribution. We have also seen this with Intel’s move to sell a majority stake in Altera earlier this year.

Honestly, Intel’s recent moves have been necessary. Intel couldn’t continue spending as it did on its foundry projects. If they did, the company would be over if it failed to attract large foundry customers. Regardless, Intel’s foundry spending wasn’t a waste. 18A will enable Intel to bring manufacturing in-house, and that will allow Intel to increase its profitability in the short term. Furthermore, 14A still has the potential to attract 3rd party customers.

Will Lip-Bu Tan turn Intel around? Who knows… He is making significant changes, but it will take years for these changes to have a major impact on Intel’s products. After all, it takes years to design new processors.

You can join the discussion on Intel’s Q2 earnings on the OC3D Forums.